A $180 Million Picasso: What’s Making the Art Market Sizzle

The art market is hotter than a hoisted Rembrandt.

Last night at Christie’s in New York, Picasso’s “Les Femmes d’Alger (Version O)” sold for almost $180 million – the highest price ever paid at auction for a piece of art. There were said to be five bidders, and the winner remains anonymous.

At the same sale, a Giacometti sculpture, “L’homme au doigt,” went for a total of more than $141 million.

On May 5, at the first major auction of the spring selling season, Sotheby’s pulled in $368 million. It was the second-highest sale of Impressionist and modern art in the history of the auction house, according to The New York Times. The top seller was van Gogh’s “L’allée Des Alyscamps,” which fetched $66.3 million.

Related: 6 Traits of an Emerging Millionaire. Are you one?

The haul represented a 67 percent increase over Sotheby’s spring sale a year earlier, according to Bloomberg, which noted that many of the buyers were Asian.

The May 5 auction was only the second-highest because Sotheby’s held a sale last November that took in $422 million.

And tonight at a Sotheby’s auction of contemporary art, a painting entitled “The Ring (Engagement)” by the Pop artist Roy Lichtenstein could sell for as much as $50 million, the Times said.

What’s behind all those staggering numbers?

About a year and a half ago, the columnist Felix Salmon (then at Reuters, now at Fusion) ruminated about whether there was a bubble, which he defined as often driven by FOMO (fear of missing out), or a speculative bubble, one fueled by flippers, in the art market. His conclusion: the art market bubble was definitely not speculative.

“The people spending millions of dollars on trophy art aren’t buying to flip…,” he wrote.

Related: Get Ready for Another Real Estate Bubble

Still, Salmon said he was seeing signs that the market could be turning speculative. But they may have been false signals.

Recently, The Wall Street Journal wrote: “Spurred by the momentum of several successful sale seasons and an influx of newly wealthy global bidders, the major auction houses…say demand for status art is at historic levels and shows no signs of tapering off.”

But why?

In an April 17 article, the global news website Worldcrunch asked Financial Times journalist Georgina Adam, who wrote the 2014 book Big Bucks—The Explosion of the Art Market in the 21st Century, why so much money is rolling around the art market and driving up prices.

“Rich people used to be rich in terms of estate or assets, but not so much in terms of cash, like they are today,” she said.

“This growing billionaire population from developed or developing economies has money to spend and invest,” said the Worldcrunch article by Catherine Cochard. “For many of them, art — in the same way as luxury cars or prêt-à-porter — is an entry pass to a globalized way of life accessible through their wealth.”

That is a development that the keen eyes at the auction houses haven’t missed.

Trump: Repeal the Obamacare Mandate to Cut the Top Tax Rate

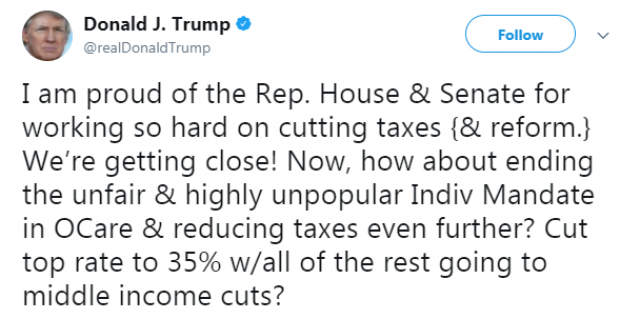

President Trump repeated his call Monday to repeal the Affordable Care Act’s individual mandate as part of the tax bill. In a tweet — geotagged from Pennsylvania, not the Philippines , where Trump currently is — Trump added that the billions in savings from ending the mandate should be used to cut the top marginal rate to 35 percent and the rest on cuts for the middle class.

The Congressional Budget Office said last week that eliminating the mandate would save $338 billion over the next decade.

The current version of the House tax bill keeps the top individual income tax rate at 39.6 percent, while the Senate bill lowers it to 38.5 percent. However, mandate repeal is not currently part of either tax bill, and, as The New York Times notes, “repeal of the individual mandate was not on the list of 355 amendments that the [Senate Finance Committee] released on Sunday night.”

Tax Reform Is Hard, but the GOP Could Have Made This Easier

The Tax Policy Center’s William G. Gale writes that the GOP’s approach to the tax bill combines a $5.8 trillion tax cut with a $4.3 trillion tax increase to offset the costs. There may have been an easier way. “What if the House GOP simply tried to cut business and individual taxes by $1.5 trillion. No offsets needed. They could have distributed small tax cuts to middle-income individuals by, say, modestly expanding the earned income tax credit and raising the standard deduction. And they could have trimmed the top corporate tax rate by a few percentage points. It would not have been base-broadening tax reform, but neither is the current bill. ... Tax reform is never easy, but crafting the bill this way has vastly increased the challenge of passing it.”

Alan Greenspan: Deal with the National Debt Before Cutting Taxes

Former Federal Reserve Chairman Alan Greenspan is warning that sharply cutting taxes right now would be an economic “mistake.”

In an interview with Maria Bartiromo on the Fox Business Network Thursday, the 91-year-old Greenspan said it’s more important for President Trump and Congress to put the nation on a sustainable fiscal path by addressing rising entitlement spending driven by the aging of the U.S. population.

“Frankly, I think what we ought to be concerned about is the fact the federal debt is rising at a very rapid pace, and there’s nothing in this bill that will essentially stop that from happening," Greenspan said. "So my view is that we’re premature on fiscal stimulus, whether it’s tax cuts or expenditure increases. We’ve got to get the debt stabilized before we can even think in those terms.”

GOP’s Estate-Tax Repeal Details Would Save Super-Rich Tens of Billions Extra

It’s no surprise that the House Republicans’ tax bill includes the eventual repeal of the estate tax, a long-held GOP goal. But The Washington Post’s Glenn Kessler highlights an unexpectedly generous aspect of the current bill: It “allows the beneficiaries of estates to not pay capital gains taxes on the increase in value of assets held by the estates. That has not been a feature of most previous estate-tax bills.”

Currently, estates face a federal tax if they’re valued at more than $5.49 million for individuals or almost $11 million for couples. But, for tax purposes, the value of assets passed on to heirs gets “stepped-up” or reset to their value at the time of death. Kessler’s example: “Imagine a home that had been purchased for $250,000 but was now worth $1 million. The ‘stepped-up basis’ would be $1 million. If the heirs sold the house for $1.1 million, they would only owe capital-gains tax on the $100,000 difference, not the $850,000 difference from the original purchase price.”

The GOP bill repeals the estate tax, but also keeps the stepped-up basis — a seemingly small detail that creates a huge tax shelter. It means that heirs of large estates would save tens of billions of dollars a year when they sell assets that have appreciated in value over time — or, as Kessler puts it, that the bill will allow “tens of billions of untapped capital gains to remain beyond the reach of the U.S. government.”

Republicans Are Still Coming After Obamacare’s Individual Mandate

walks to a a news conference after Republicans pulled the American Health Care Act bill to repeal and replace the Affordable Care Act act known as Obamacare, prior to a vote at the U.S. Capitol in Washington, March 24, 201")

Speaker Paul Ryan said Sunday that House Republicans are still considering a repeal of the Obamacare individual mandate as part of their tax bill. "We have an active conversation with our members and a whole host of ideas on things to add to this bill. And that’s one of the things that’s being discussed," Ryan said on Fox News. President Trump touted the idea in a tweet last week, and Sens. Tom Cotton and Rand Paul have recently spoken in favor of using the tax bill to eliminate the mandate. The move would save the government $416 billion over 10 years as roughly 15 million people go without insurance due to lower spending on subsidies and health care services, according to the CBO. Those savings could be appealing as Republicans look for revenues in their revised tax bill. But if the controversial repeal of the mandate isn’t included in the tax bill, the White House is reportedly ready to roll out an executive order weakening the requirement that taxpayers provide proof of insurance to avoid paying a penalty.