Bloomberg for President? Today There Was a Telling Tweet

Who is the only person who could nail the Democratic nomination for president if Hillary Rodham Clinton falters? According to USA Today columnist Michael Wolff, it’s not declared candidate Sen. Bernie Sanders of Vermont or about-to-declare former Maryland Gov. Martin O’Malley or progressive champion Sen. Elizabeth Warren of Massachusetts.

Nobody has the cash — which Wolff pegs at close to $2 billion — that would be required to mount a competitive race except for one potential candidate who been down the “will he or won’t he?” road before: former New York Mayor Michael Bloomberg. Wolff calls the self-made billionaire the obvious and only alternative because of his money, first and foremost, but also because of his “progressive social conscience with pro-growth-economic views.”

Related: Is America Ready for a Liberal Rock ‘n Roll President?

Of course, there is no reason to take Wolff seriously. Since leaving City Hall, Bloomberg has been busy reestablishing his direct control over Bloomberg L.P., the financial data and media behemoth he founded, and he hasn’t even offered a tease about possibly running.

But this morning, the Wolff column was tweeted out by Kevin Sheekey, who managed Bloomberg’s three winning campaigns for mayor. Sheekey, a former deputy mayor, is currently head of government relations and communications at Bloomberg.

“Next February say, if the sky falls in on Hillary — one or more of the storm-cloud scenarios breaking over her head — would Michael Bloomberg step up?” Wolff asks.

Kevin Sheekey probably knows the answer.

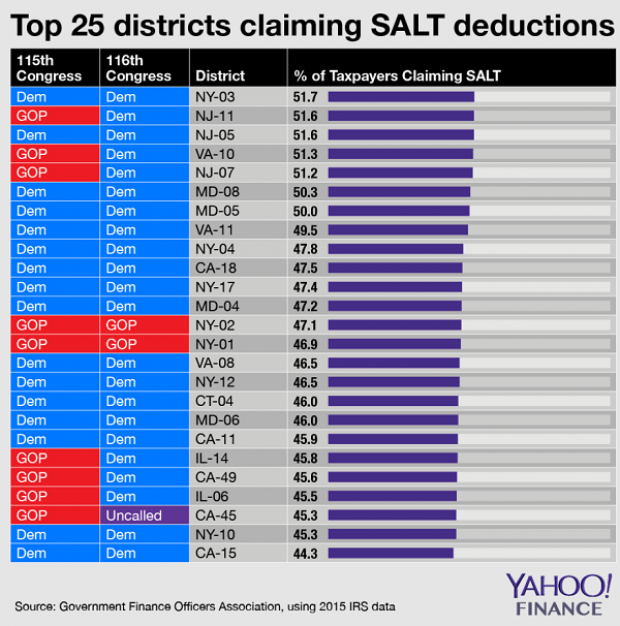

Chart of the Day: SALT in the GOP’s Wounds

The stark and growing divide between urban/suburban and rural districts was one big story in this year’s election results, with Democrats gaining seats in the House as a result of their success in suburban areas. The GOP tax law may have helped drive that trend, Yahoo Finance’s Brian Cheung notes.

The new tax law capped the amount of state and local tax deductions Americans can claim in their federal filings at $10,000. Congressional seats for nine of the top 25 districts where residents claim those SALT deductions were held by Republicans heading into Election Day. Six of the nine flipped to the Democrats in last week’s midterms.

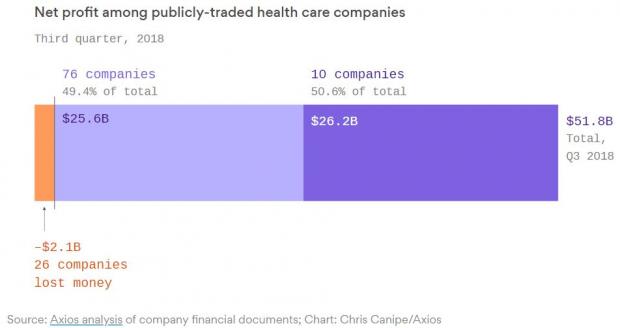

Chart of the Day: Big Pharma's Big Profits

Ten companies, including nine pharmaceutical giants, accounted for half of the health care industry's $50 billion in worldwide profits in the third quarter of 2018, according to an analysis by Axios’s Bob Herman. Drug companies generated 23 percent of the industry’s $636 billion in revenue — and 63 percent of the total profits. “Americans spend a lot more money on hospital and physician care than prescription drugs, but pharmaceutical companies pocket a lot more than other parts of the industry,” Herman writes.

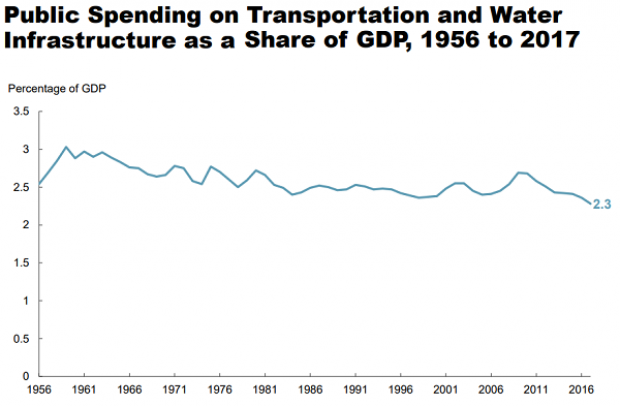

Chart of the Day: Infrastructure Spending Over 60 Years

Federal, state and local governments spent about $441 billion on infrastructure in 2017, with the money going toward highways, mass transit and rail, aviation, water transportation, water resources and water utilities. Measured as a percentage of GDP, total spending is a bit lower than it was 50 years ago. For more details, see this new report from the Congressional Budget Office.

Number of the Day: $3.3 Billion

The GOP tax cuts have provided a significant earnings boost for the big U.S. banks so far this year. Changes in the tax code “saved the nation’s six biggest banks $3.3 billion in the third quarter alone,” according to a Bloomberg report Thursday. The data is drawn from earnings reports from Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Wells Fargo.

Clarifying the Drop in Obamacare Premiums

We told you Thursday about the Trump administration’s announcement that average premiums for benchmark Obamacare plans will fall 1.5 percent next year, but analyst Charles Gaba says the story is a bit more complicated. According to Gaba’s calculations, average premiums for all individual health plans will rise next year by 3.1 percent.

The difference between the two figures is produced by two very different datasets. The Trump administration included only the second-lowest-cost Silver plans in 39 states in its analysis, while Gaba examined all individual plans sold in all 50 states.