Millennials Like Saving Money, Want to Save More

Millennials have impressive financial habits when compared to baby boomers, according to a new Retirement Saving & Spending Study by T. Rower Price. Millennials like to save, with many taking advantage of 401(k) plans while still paying down debt. On average, millennials are saving nearly as much for retirement -- 8 percent of their incomes -- as baby boomers, who are saving an average of 9 percent. And in the past 12 months, millennials are saving a higher percentage of their incomes than baby boomers when it comes to 401(k) contributions.

The research is based on online interviews with 1,505 millennials and 514 baby boomers with 401(k)s, and includes both workers and retirees.

Overall, millennials in the study report they are in surprisingly good financial shape. Eighty-eight percent say they are living within their means and 74 percent are more comfortable saving and investing extra money than spending it. However, many millennials are pessimistic about Social Security: Sixty percent expect Social Security to go bankrupt before they retire.

Here’s what else the survey reveals:

Millennials like to save, and they’d save more if they could.

Saving for retirement and paying down debt are equally important to millennials, who rank both goals as a top priority. For those who say they are not saving enough, 23 percent cited student loans as a major contributing factor.

Related Link: ‘Irresponsible’ Millennials Saving More Than Almost Every Other Group

Millennials like auto-enrollment plans.

Seventy-nine percent of the millennials who were auto-enrolled in 401(k) plans were satisfied with auto-enrollment. When it comes to 401(k) matches, 59 percent of millennials set their 401(k) contribution rate to take full advantage of their employers’ matches.

They’re open to advice and more likely to ask for help if they need it.

If faced with a sudden financial emergency, 55 percent of millennials said they’d seek the help of family and friends, compared to 24 percent of baby boomers. Millennials were also much more likely to admit they could benefit from help with spending and debt management.

They find it hard to save when they make less money.

Non-savers made less money and carried more student debt. The median personal income of non-savers was $28,000, compared to $57,000 for savers. Thirty-nine percent of the non-savers have trouble meeting their monthly expenses.

Men save more.

Millennial women are less likely to save in 401(k)s, even if they are eligible, and when they do, they save less than men. The average 401(k) balance for women participating in their 401(k) is $38,000, compared to an average 401(k) balance of $74,000 for men. Of those who are already participating in 401(k)s, only 41 percent of the savers are women.

Related link: Here Are 7 Ways People Screw Up Their 401(k)s

Deficit Hits $738.6 Billion in First 8 Months of Fiscal Year

The U.S. budget deficit grew to $738.6 billion in the first eight months of the current fiscal year – an increase of $206 billion, or 38.8%, over the deficit recorded during the same period a year earlier. Bloomberg’s Sarah McGregor notes that the big increase occurred despite a jump in tariff revenues, which have nearly doubled to $44.9 billion so far this fiscal year. But that increase, which contributed to an overall increase in revenues of 2.3%, was not enough to make up for the reduced revenues from the Republican tax cuts and a 9.3% increase in government spending.

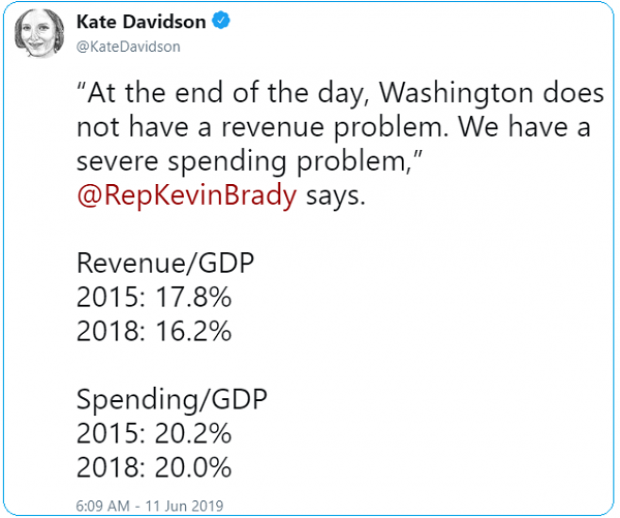

Tweet of the Day: Revenues or Spending?

Rep. Kevin Brady (R-TX), ranking member of the House Ways and Means Committee and one of the authors of the 2017 Republican tax overhaul, told The Washington Post’s Heather Long Tuesday that the budget deficit is driven by excess spending, not a shortfall in revenues in the wake of the tax cuts. The Wall Street Journal’s Kate Davidson provided some inconvenient facts for Brady’s claim in a tweet, pointing out that government revenues as a share of GDP have fallen significantly since 2015, while spending has remained more or less constant.

Chart of the Day: The Decline in IRS Audits

Reviewing the recent annual report on tax statistics from the IRS, Robert Weinberger of the Tax Policy Center says it “tells a story of shrinking staff, fewer audits, and less customer service.” The agency had 22% fewer personnel in 2018 than it did in 2010, and its enforcement budget has fallen by nearly $1 billion, Weinberger writes. One obvious effect of the budget cuts has been a sharp reduction in the number of audits the agency has performed annually, which you can see in the chart below.

Number of the Day: $102 Million

President Trump’s golf playing has cost taxpayers $102 million in extra travel and security expenses, according to an analysis by the left-leaning HuffPost news site.

“The $102 million total to date spent on Trump’s presidential golfing represents 255 times the annual presidential salary he volunteered not to take. It is more than three times the cost of special counsel Robert Mueller’s investigation that Trump continually complains about. It would fund for six years the Special Olympics program that Trump’s proposed budget had originally cut to save money,” HuffPost’s S.V. Date writes.

Date says the White House did not respond to HuffPost’s requests for comment.

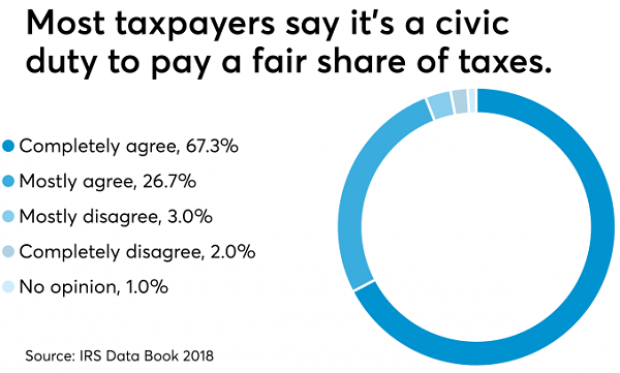

Americans See Tax-Paying as a Duty

The IRS may not be conducting audits like it used to, but according to the agency’s Data Book for 2018, most Americans still believe it’s not acceptable to cheat on your taxes. About 67% of respondents to an IRS opinion survey “completely agree” that it’s a civic duty to pay “a fair share of taxes,” and another 26% “mostly agree,” bringing the total in agreement to over 90%. Accounting Today says that attitude has been pretty consistent over the last decade.