Millennials Still Don’t Trust the Stock Market

Goldman Sachs has released the latest in a long line of surveys about millennials and money. The findings won’t shock you if you’ve seen other such surveys: millennials get financial advice from their parents, they’re less concerned with privacy, they still want to own a home … someday.

But one familiar finding may be worth highlighting. Even as the stock market reaches record highs, millennials by and large remain wary of investing. Fewer than 20 percent of those surveyed by Goldman said that stocks are “the best way to save for the future.” Another 45 percent said they’re willing to dip a toe in the market or to put money into low-risk options. More than a third of those surveyed said they don’t know enough about stocks or felt that the market is too volatile or too stacked against small investors.

Part of that may because many millennials haven’t yet reached the life stage or the level of financial stability that would lead them to consider investing. But the lingering scars of the recession are evident in the results, too — and financial institutions clearly have a long way go to restore the public’s confidence in them. For example, Gallup just published a report called, “Why It’s Still Cool to Hate Banks.”

Related: The Rise of a New Economic Underclass—Millennial Men

Goldman didn’t release the details about how many millennials it surveyed or when (and it hadn’t yet responded to an email asking for those details by the time of publication), but the results it got are broadly in line with those of earlier surveys. And they’re another reminder that not everyone is benefitting from the stock market’s record-setting rally. Millennials are still missing out.

Here is a chart produced by Goldman Sachs summarizing the results of their survey:

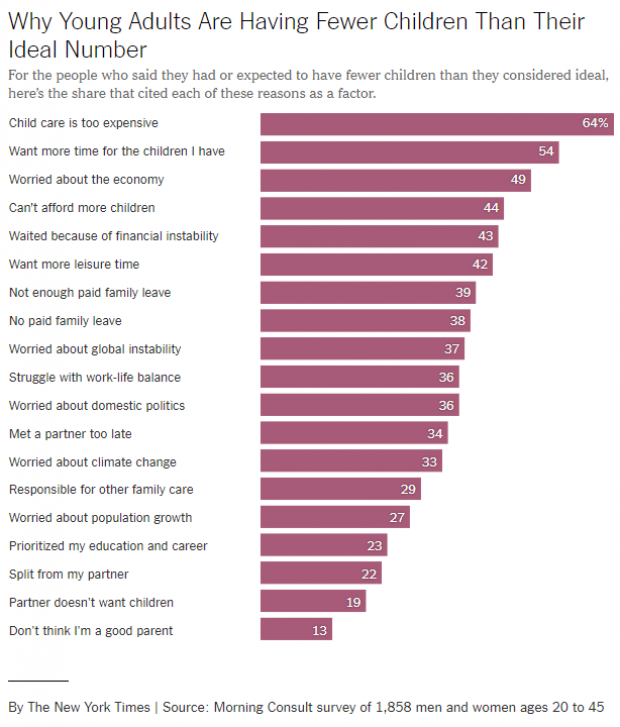

Chart of the Day: Why US Fertility Rates Are Falling

Babysit")

U.S. fertility rates have fallen to record lows for two straight years. “Because the fertility rate subtly shapes many major issues of the day — including immigration, education, housing, the labor supply, the social safety net and support for working families — there’s a lot of concern about why today’s young adults aren’t having as many children,” Claire Cain Miller explains at The New York Times’ Upshot. “So we asked them.”

Here are some results of the Times’ survey, conducted with Morning Consult. Read the full Times story for more details.

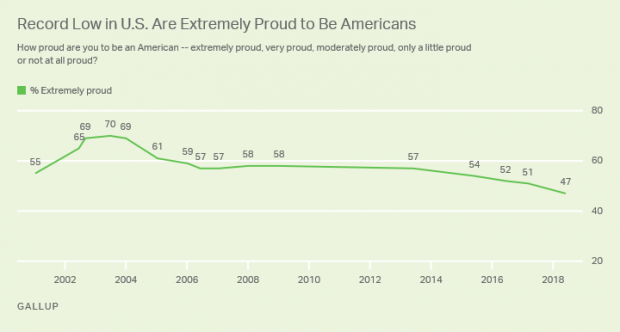

A Record Low 47% of US Adults Say They're 'Extremely Proud' to Be American

Gallup says that, for the first time in the 18 years it’s been asking U.S. adults how proud they are to be Americans, fewer than half say they are "extremely proud." Just 47 percent now say they’re extremely proud, down from 70 percent in 2003.

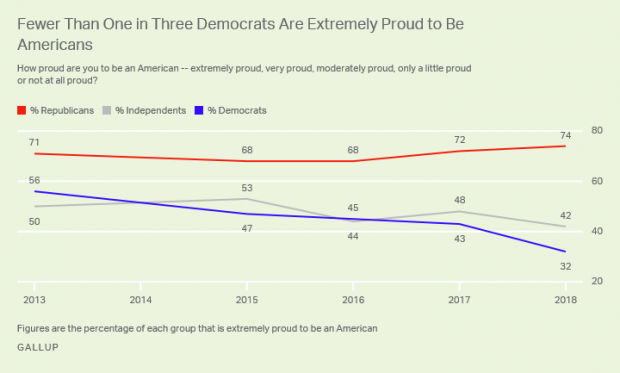

Another 25 percent say they’re “very proud” — but the combined 72 percent who say they’re extremely or very proud is also the lowest Gallup has recorded. Pride levels among liberals and Democrats have plunged since 2017. Overall, 74 percent of Republicans and just 32 percent of Democrats call themselves “extremely proud” to be American.

Pfizer Has Raised Prices on 100 of Its Products

Weeks after President Trump said that drugmakers were about to implement “voluntary massive drops in prices” — reductions that have yet to materialize — Pfizer has raised prices on 100 of its products, The Financial Times’s David Crow reports:

“The increases were effective as of July 1 and in most cases were more than 9 per cent — well above the rate of inflation in the US, which is running at about 2 per cent. … Pfizer, the largest standalone drugmaker in the US, did decrease the prices of five products by between 16 per cent and 44 per cent, according to the figures.”

Crow notes that Pfizer also raised prices on many of its medicines in January, meaning that some prices have been hiked by nearly 20 percent this year. The drugmaker said that it was only changing prices on 10 percent of its medicines and that list prices did not reflect what most patients or insurers actually paid. The net price increase after rebates and discounts was expected to be in the “low single digits,” the company told the FT.

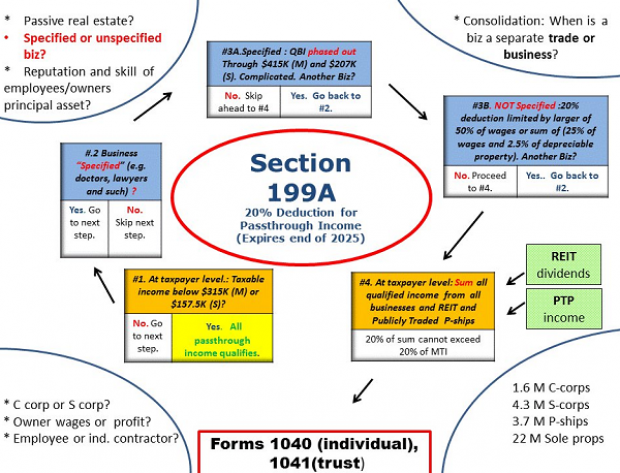

Chart of the Day: Pass-Through Tax Deductions Made Easy

The Republican tax overhaul was supposed to simplify the tax code, but most experts say it fell well short of the goal. Martin Sullivan, chief economist at Tax Analysts, tweeted out a chart of the analysis required to determine whether income qualifies for the passthrough tax deduction of 20 percent, and as you’ll see, it’s anything but simple.

A Conservative Bashes GOP Dysfunction on Spending Cuts

Brian Riedl, a senior fellow at the conservative Manhattan Institute, offers a blistering critique of congressional Republican’s problems cutting spending:

Since the Republicans took the House in 2011, nearly every annual budget blueprint has promised to balance the budget within a decade with anywhere from $5 trillion to $8 trillion in spending cuts. And yet, you may have noticed, the budget has not moved towards balance. This is because the budget merely sets a broad fiscal goal. To actually cut spending, Congress must follow up with specific legislation to reform Medicare, Medicaid, and all the other targeted programs. In reality, most lawmakers who pass these budgets have no intention whatsoever of cutting this spending. As soon as the budget is passed, the targets are forgotten. The spending-cut legislation is never even drafted, much less voted on.

The annual budget exercise is thus a cynical exercise in symbolism. Congress calculates how much spending must be cut over ten years to balance the budget. Then they pass legislation setting a goal of cutting that amount. Then they move on to other business. It’s like a baseball team announcing that they voted to win the next World Series, and then not showing up to play the season.

Read the full piece at National Review.