5 Cities with the Most Credit Card Debt

Why is the Lone Star State racking up so much debt? Its two largest cities—Dallas and Houston/Fort Worth make the list of the cities with the most credit card debt, and San Antonio comes in as No. 1.

The new study from CreditCards.com used credit report data from Experian to compare the average credit card debt in the 25 largest U.S. metro areas with each area’s median income. It assumed that 15 percent of a person's monthly income would be spent on paying down credit card debt.

The analysis claims it would take San Antonio residents with median incomes of $27,491 a full 16 months to pay off an average of $4,880, making monthly payments of $344 a month. By comparison, a resident of San Francisco making $42,613 a year would pay off $4,393 in credit card debt with nine monthly payments of $533 per month.

The cities with the highest credit card debt burdens were:

- San Antonio

- Dallas/Fort Worth

- Atlanta

- Miami/Fort Lauderdale

- Houston

Related: 5 Reasons to Pay Off Your Credit Card Debt Now

The metro areas with the highest debt don’t necessarily have the highest debt burdens when adjusted for income. For example, Washington, D.C. has the nation’s highest average credit card debt at $5,046, but since it also has the highest median income in the nation, its debt burden is lower. By applying 15 percent of their paychecks, residents can pay off that debt in 10 months.

The cities with the lowest credit card debt burdens were:

- New York City

- Minneapolis/St. Paul

- Washington, D.C.

- Boston

- San Francisco/Oakland/San Jose

Matt Schulz, senior industry analyst at CreditCards.com, points out that there isn’t much difference between the city with the highest credit card debt, Washington, D.C. ($5,046), and the city with the lowest credit card debt, the Riverside-San Bernardino area ($4,137), but there is a big difference in income. A higher income means that debts can be paid off more quickly. “It really is all about earnings,” Schulz says. “People are using their credit cards whether they live in the biggest city in the country or they live in the 25th biggest city in the country.”

While most folks won’t be able to increase their income that dramatically, there are still steps they can take to make sure they’re tackling their credit card debt in the most effective way possible.

Related: How to Defuse Exploding Consumer Credit Debt

His advice to consumers? “Absolutely, positively pay more than the minimum on your credit card balance every month.” And the next best thing? “If you can’t pay the full balance, then you have to pay off more than the minimum.”

Schulz also recommends calling the credit card issuer and asking if you can get better terms. “It’s certainly worth a call,” says Schulz. “We did a study last year that showed that 65 percent of people who asked for a lower interest rate got a lower APR.” The same study said that 86 percent of people who asked for a waiver of a late payment fee were successful in getting the charge removed.

Top Reads from The Fiscal Times:

- The Next Debt Crisis Could Be Much Worse than in 2013, GAO Warns

- The New Generation of ‘Genuinely Creepy’ Electronic Devices

- 9 Social Security Tips You Need to Know Right Now

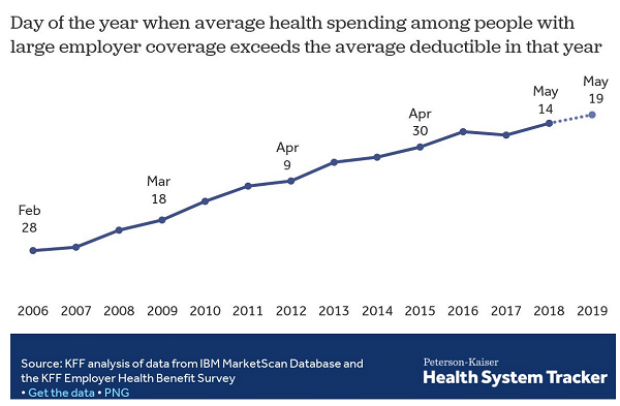

Coming Soon: Deductible Relief Day!

You may be familiar with the concept of Tax Freedom Day – the date on which you have earned enough to pay all of your taxes for the year. Focusing on a different kind of financial burden, analysts at the Kaiser Family Foundation have created Deductible Relief Day – the date on which people in employer-sponsored insurance plans have spent enough on health care to meet the average annual deductible.

Average deductibles have more than tripled over the last decade, forcing people to spend more out of pocket each year. As a result, Deductible Relief Day is “getting later and later in the year,” Kaiser’s Larry Levitt said in a tweet Thursday.

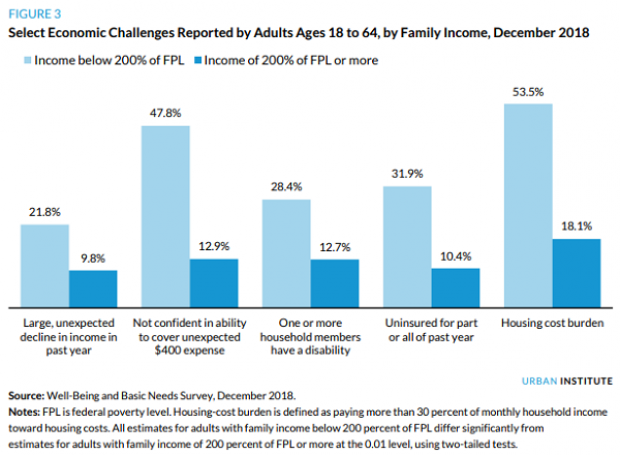

Chart of the Day: Families Still Struggling

Ten years into what will soon be the longest economic expansion in U.S. history, 40% of families say they are still struggling, according to a new report from the Urban Institute. “Nearly 4 in 10 nonelderly adults reported that in 2018, their families experienced material hardship—defined as trouble paying or being unable to pay for housing, utilities, food, or medical care at some point during the year—which was not significantly different from the share reporting these difficulties for the previous year,” the report says. “Among adults in families with incomes below twice the federal poverty level (FPL), over 60 percent reported at least one type of material hardship in 2018.”

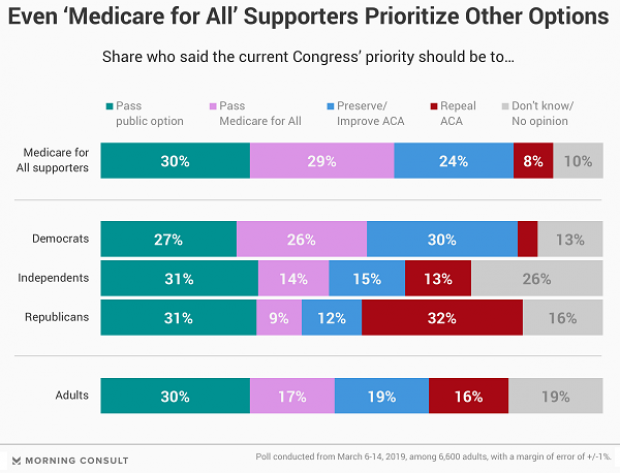

Chart of the Day: Pragmatism on a Public Option

A recent Morning Consult poll 3,073 U.S. adults who say they support Medicare for All shows that they are just as likely to back a public option that would allow Americans to buy into Medicare or Medicaid without eliminating private health insurance. “The data suggests that, in spite of the fervor for expanding health coverage, a majority of Medicare for All supporters, like all Americans, are leaning into their pragmatism in response to the current political climate — one which has left many skeptical that Capitol Hill can jolt into action on an ambitious proposal like Medicare for All quickly enough to wrangle the soaring costs of health care,” Morning Consult said.

Chart of the Day: The Explosive Growth of the EITC

The Earned Income Tax Credit, a refundable tax credit for low- to moderate-income workers, was established in 1975, with nominal claims of about $1.2 billion ($5.6 billion in 2016 dollars) in its first year. According to the Tax Policy Center, by 2016 “the total was $66.7 billion, almost 12 times larger in real terms.”

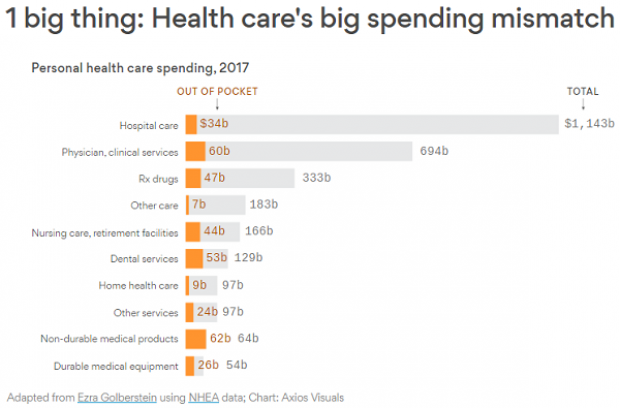

Chart of the Day: The Big Picture on Health Care Costs

“The health care services that rack up the highest out-of-pocket costs for patients aren't the same ones that cost the most to the health care system overall,” says Axios’s Caitlin Owens. That may distort our view of how the system works and how best to fix it. For example, Americans spend more out-of-pocket on dental services ($53 billion) than they do on hospital care ($34 billion), but the latter is a much larger part of national health care spending as a whole.