Don’t Feel Like a Chump When You Close on Your New Mortgage

Mortgage closing costs dropped 7 percent over the past year, falling to $1,847 on a $200,000 loan, according to a new analysis by Bankrate.

Typical closing costs varied by state, ranging from $2,163 in Hawaii to $1,613 in Ohio. You can find the average rate for your state in the table below.

Lenders compete for business, so shopping around with at least three mortgage providers can help you reduce the fees associated with your loan. “Homebuyers have more say over closing costs than they think,” Bankrate Senior Mortgage Analyst Holden Lewis said in a statement.

Even as banks lower their mortgage fees, they’re increasing fees in most other categories, according to MoneyRates.com.

While lower mortgage fees are good news for homebuyers and those refinancing their loans, the average saving amount to just $140. That’s not much relative to the total costs associated with buying a house. The average down payment for homebuyers in the first quarter of 2015 was $57,710, for example.

Related: Want Your Own Home? Here’s How to Do the Math

The costs don’t stop once the buyers move in. On top of mortgage payments, homeowners face an average of more than $6,000 in additional costs related to their house, including homeowners insurance, property taxes and utilities.

The National Association of Realtors expects home prices to increase 6.5 percent this year to a median $221,900, which would put them at the same level as their 2006 record high.

For buyers, better news than the lower mortgage fees is that rates remain relatively low, falling to 3.98 percent last week, per Freddie Mac.

Closing costs | |||

|---|---|---|---|

| State | Average origination fees | Average third-party fees | Average origination plus third-party fees |

| Alabama | $1,066 | $776 | $1,842 |

| Alaska | $935 | $922 | $1,857 |

| Arizona | $1,208 | $761 | $1,969 |

| Arkansas | $1,057 | $760 | $1,817 |

| California | $937 | $896 | $1,834 |

| Colorado | $1,192 | $719 | $1,910 |

| Connecticut | $1,074 | $960 | $2,033 |

| Delaware | $904 | $924 | $1,828 |

| District of Columbia | $1,077 | $718 | $1,794 |

| Florida | $1,028 | $778 | $1,806 |

| Georgia | $1,058 | $821 | $1,879 |

| Hawaii | $1,033 | $1,130 | $2,163 |

| Idaho | $894 | $788 | $1,682 |

| Illinois | $1,080 | $767 | $1,847 |

| Indiana | $1,067 | $770 | $1,837 |

| Iowa | $1,161 | $762 | $1,923 |

| Kansas | $1,047 | $753 | $1,800 |

| Kentucky | $1,060 | $737 | $1,797 |

| Louisiana | $1,060 | $817 | $1,877 |

| Maine | $897 | $830 | $1,727 |

| Maryland | $1,093 | $742 | $1,835 |

| Massachusetts | $905 | $851 | $1,756 |

| Michigan | $1,072 | $746 | $1,818 |

| Minnesota | $1,067 | $689 | $1,757 |

| Mississippi | $1,046 | $837 | $1,884 |

| Missouri | $1,040 | $792 | $1,833 |

| Montana | $1,062 | $855 | $1,917 |

| Nebraska | $1,047 | $770 | $1,817 |

| Nevada | $1,002 | $848 | $1,850 |

| New Hampshire | $1,084 | $750 | $1,835 |

| New Jersey | $1,181 | $913 | $2,094 |

| New Mexico | $1,076 | $876 | $1,952 |

| New York | $1,032 | $879 | $1,911 |

| North Carolina | $1,036 | $875 | $1,911 |

| North Dakota | $1,045 | $791 | $1,836 |

| Ohio | $933 | $681 | $1,613 |

| Oklahoma | $1,027 | $734 | $1,761 |

| Oregon | $1,080 | $785 | $1,864 |

| Pennsylvania | $1,055 | $678 | $1,733 |

| Rhode Island | $1,093 | $802 | $1,896 |

| South Carolina | $1,058 | $837 | $1,895 |

| South Dakota | $1,055 | $704 | $1,759 |

| Tennessee | $1,033 | $773 | $1,806 |

| Texas | $1,031 | $833 | $1,864 |

| Utah | $909 | $788 | $1,697 |

| Vermont | $1,074 | $862 | $1,936 |

| Virginia | $1,050 | $787 | $1,837 |

| Washington | $1,077 | $824 | $1,901 |

| West Virginia | $1,067 | $904 | $1,971 |

| Wisconsin | $1,047 | $723 | $1,770 |

| Wyoming | $874 | $814 | $1,689 |

| Average | $1,041 | $807 | $1,847 |

Bankrate.com surveyed up to 10 lenders in each state in June 2015 and obtained online Good Faith Estimates for a $200,000 mortgage to buy a single-family home with a 20 percent down payment in a prominent city. Costs include fees charged by lenders, as well as third-party fees for services such as appraisals and credit reports. The survey excludes title insurance, title search, taxes, property insurance, association fees, interest and other prepaid items.

Top Reads from The Fiscal Times:

- You’re Richer Than You Think. Really.

- The 10 Fastest-Growing Jobs Right Now

- The 5 Worst Cities to Raise a Family

Trump’s Cabinet Would Benefit from Tax Plan Too

“Eliminating the estate tax would save the Trump Cabinet over a billion dollars," Oliver Willis writes. "Like Mnuchin, Trump’s secretaries would make out like bandits. Commerce Secretary Wilbur Ross would get an extra $545 million. The family of Education Secretary Betsy DeVos would rake in $900 million. Linda McMahon, head of the Small Business Administration, and her husband, WWE founder Vince McMahon, would take in $250 million. Trump’s own net worth is in dispute, thanks to his failure to reveal his tax returns, but based on his estimated net worth of $3 billion, the estate tax scheme would net him $564 million.” (Shareblue Media, Bloomberg)

A Liberal Economist Shoots Down the GOP’s Fiscal Chicken Hawks

Republicans want a tax cut, but they don’t want to fully pay for it and may be willing to increase the deficit by $1.5 trillion over 10 years. This would continue a troubling cycle, economist Jared Bernstein writes, in which supposed fiscal conservatives “use the deficit argument to block spending, promote fiscal austerity, and small government, conveniently tossing deficit concerns aside when it comes to tax cuts.”

You’ll hear arguments about how increased economic growth will make up for the budgetary effects of the tax cuts, but don’t believe them. “Our fiscal history on this point is clear: Cutting taxes loses revenues, which, unless offset by higher taxes elsewhere or spending cuts, increases the budget deficit, which in turn raises the debt.” When this happens again, and the promised growth effects don’t materialize, the tax cutters will go back to pushing for spending cuts.

The country faces a number of serious challenges, including an aging population that by itself will require increased government spending, and we need a tax policy that does more than drive up the deficit. “The problem with structural deficits — ones that go up even in good times — is that they reveal that we’re unwilling to raise the necessary revenues to support the government we want and need. This enables those who whose goal is to shrink government to point to deficits and debt as their proof that we can’t afford it, whatever ‘it’ is, except when ‘it’ is tax cuts.” (New York Times)

Health Secretary Tom Price Under Fire for Use of Private Jets

listens to opening remarks prior to testifying before a Senate Finance Committee confirmation hearing on his nomination to be Health and Human Services secretary on Capitol Hill in Washington, U.S., January 24, 2017. REUTERS/Car")

Back in 2009, Tom Price spoke out against House Democrats who wanted to spend $550 million on private jets for lawmakers to use. A Republican representative from Georgia at the time, Price told CNBC that the purchase of the jets was “another example of fiscal irresponsibility run amok.” Now Secretary of Health and Human Services, Price seems to have changed his mind about the virtue of government officials using private jets at taxpayer expense. Just last week, Price used a chartered private jet to travel to three HHS events — including one at a resort in Maine — at an estimated cost of $60,000, Politico reports.

While previous HHS secretaries typically flew commercial, reports indicate that Price has been traveling by private jet for months. “Official travel by the secretary is done in complete accordance with Federal Travel Regulations,” an HHS spokesperson told Politico.

Critics on Twitter have been harsh:

More in-your-face kleptocracy from Tom Price.Take food stamps from poor, hungry kids- spend $25k from taxpayers to charter plane to Philly

— Norman Ornstein (@NormOrnstein) September 20, 2017

1️⃣ Attack Medicaid while trading health stocks.

— Harry Stein (@HarrySteinDC) September 20, 2017

2️⃣ Spend funds that could give someone 4 years of Medicaid coverage to fly a private jet. https://t.co/GO5cfJgWgO

First Mnuchin, now Tom Price. The @realDonaldTrump Cabinet has a big problem charging taxpayers for private flights. https://t.co/th1QbGdfT7

— Ben White (@morningmoneyben) September 20, 2017

Social Security Benefits Due for a Bigger Bump in 2018

In a few weeks the Social Security Administration will announce its cost-of-living adjustment, or COLA, for 2018. Inflation data for the month of August suggests that the adjustment could be the highest in five years, possibly over 2 percent, according to the Washington Examiner. Adjustments for the past five years have been relatively small: The cost of living adjustment for 2017 (announced last October) came in at a modest 0.3 percent, and the adjustment for 2016 was zero. Some retirees have complained in the past about small COLAs, but it’s worth remembering that higher adjustments are driven by higher inflation, which is bad news for people living on fixed incomes.

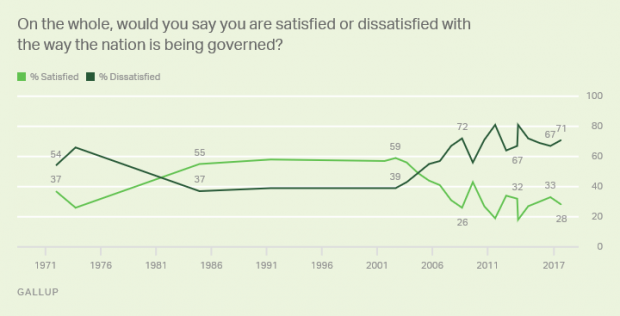

Americans Are Less Satisfied with Government Now Than a Year Ago

Gallup finds that just 28 percent of Americans are satisfied with the way the nation is being governed, down from 33 percent a year ago. And as we approach some potential fiscal battles, it's worth noting that the lowest satisfaction levels since Gallup started updating the measure annually in 2001 came in 2011 (19 percent) after a debt ceiling showdown that led to the U.S. credit rating being downgraded by S&P analysts and in 2013 (18 percent) during a federal government shutdown.