When Buying Car Insurance, Young Drivers Should Stick with Mom and Dad

The parents of young drivers have enough to worry about, but a new study from insuranceQuotes.com finds that those who add coverage for an 18-to-24-year-old can expect to see an average annual premium increase of 80 percent on their existing car insurance. The good news: That’s still cheaper than if the young drivers bought insurance on their own. If those young drivers were to buy individual plans of their own, they’d pay 8 percent more on average — and in some cases, over 50 percent more — than their coverage costs on a parental plan.

Related: The Shocking Secret About How Your Car Insurance Rate Gets Set

Premiums can vary widely depending on the driver’s age and state. An 18-year-old can expect to pay an average of 18 percent more for an individual policy than he or she would if added to an existing policy. But in Rhode Island, an 18-year-old will pay an average of 53 percent more for an individual policy. In Connecticut and Oregon, the difference is 47 percent.

In states such as Arizona, Hawaii, and Illinois, it actually becomes cheaper, on average, for a young driver to get his or her own policy after turning 19. When it comes to determining premiums, Hawaii is the only state that doesn’t allow insurance providers to consider age, gender, or length of driving experience.

These are the five states with the greatest difference in premiums for young drivers buying their own coverage.

1. Rhode Island: 19 percent

2. Connecticut: 16 percent

3. North Carolina: 14 percent

4. Vermont: 14 percent

5. Maine: 14 percent

Related: Now 16-Year-Olds Can Double Your Car Insurance

And these five states have the smallest difference:

1. Hawaii: No difference

2. Illinois: No difference

3. Arizona: 2 percent

4. Mississippi: 5 percent

5. South Carolina: 5 percent.

Top Reads from The Fiscal Times:

- As Politicians Bicker Over Funding, Military Families Cut Back on Vacations

- Why We’re Wasting Billions on Teacher Development

- The Future of War Belongs to the Bots

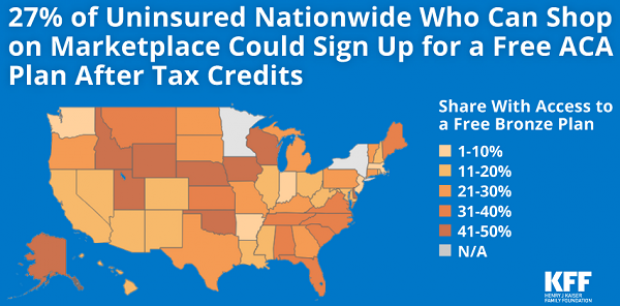

4.2 Million Uninsured People Could Get Free Obamacare Plans

About 4.2 million uninsured people could sign up for a bronze-level Obamacare health plan and pay nothing for it after tax credits are applied, the Kaiser Family Foundation said Tuesday. That means that 27 percent of the country’s 15.9 million uninsured people could get covered for free. The chart below breaks down the eligible population by state.

Takedown of the Day: Ezra Klein on Paul Ryan's Legacy of Debt

Vox’s Ezra Klein says that retiring House Speaker Paul Ryan’s legacy can be summed up in one number: $343 billion. “That’s the increase between the deficit for fiscal year 2015 and fiscal year 2018— that is, the difference between the fiscal year before Ryan became speaker of the House and the fiscal year in which he retired.”

Klein writes that Ryan’s choices while in office — especially the 2017 tax cuts and the $1.3 trillion spending bill he helped pass and the expansion of the earned income tax credit he talked up but never acted on — should be what define his legacy:

“[N]ow, as Ryan prepares to leave Congress, it is clear that his critics were correct and a credulous Washington press corps — including me — that took him at his word was wrong. In the trillions of long-term debt he racked up as speaker, in the anti-poverty proposals he promised but never passed, and in the many lies he told to sell unpopular policies, Ryan proved as much a practitioner of post-truth politics as Donald Trump. …

“Ultimately, Ryan put himself forward as a test of a simple, but important, proposition: Is fiscal responsibility something Republicans believe in or something they simply weaponize against Democrats to win back power so they can pass tax cuts and defense spending? Over the past three years, he provided a clear answer. That is his legacy, and it will haunt his successors.”

Number of the Day: $300 Million

Mick Mulvaney, the acting director of the Consumer Financial Protection Bureau, wants the agency to be known as the Bureau of Consumer Financial Protection, the name under which it was established by Title X of the 2010 Dodd-Frank Wall Street reform law. Mulvaney even had new signage put up in the lobby of the bureau. But the rebranding could cost the banks and other financial businesses regulated by the bureau more than $300 million, according to an internal agency analysis reported by The Hill’s Sylvan Lane. The costs would arise from having to update internal databases, regulatory filings and disclosure forms with the new name. The rebranding would cost the agency itself between $9 million and $19 million, the analysis estimated. Lane adds that it’s not clear whether Kathy Kraninger, President Trump’s nominee to serve as the bureau’s full-time director, would follow through on Mulvaney’s name change once she is confirmed by the Senate.

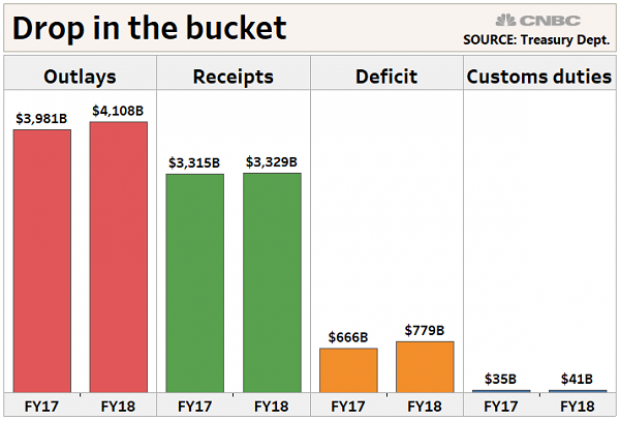

Why Trump's Tariffs Are Just a Drop in the Bucket

President Trump said this week that tariff increases by his administration are producing "billions of dollars" in revenues, thereby improving the country’s fiscal situation. But CNBC’s John Schoen points out that while tariff revenues are indeed higher by several billion dollars this year, the total revenue is a drop in the bucket compared to the sheer size of government outlays and receipts – and the growing annual deficit.

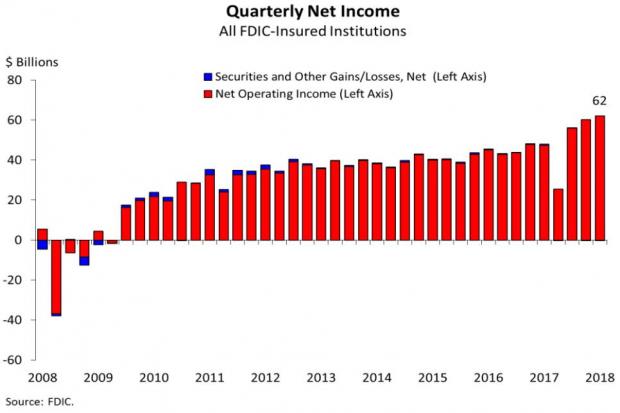

Bank Profits Hit New Record Thanks to 2017 Tax Law

Bank profits reached a record $62 billion in the third quarter, up $14 billion, or 29.3 percent, from the same period last year, according to data from the Federal Deposit Insurance Corporation. The FDIC said that about half of the increase in net income was attributable to last year’s tax cuts. The FDIC estimated that, with the effective tax rates from before the new law, bank profits for the quarter would have risen by about 14 percent, to $54.6 billion.