Automakers Are Having a Record Year, but Here’s a Trend that Should Worry Them

U.S. auto sales closed out the summer on a positive note, topping estimates and casting some rosy light on the health of the American consumer. Recording its best August since 2003, the auto industry is on pace to sell 17.8 vehicles in 2015, well ahead of expectations of 17.3 million. If the numbers hold up, 2015 will be the best year ever for U.S. auto sales, beating the 17.4 million mark set in 2000.

The general consensus is that auto industry is in pretty good shape these days. Gas prices and interest rates are low, boosting the market for cars and light trucks. More than 2 million jobs were added to the U.S. economy in the past year, and more jobs is usually good news for auto sales. The unemployment rate has been trending lower for five years, sitting at a relatively healthy 5.3 percent in July.

Related: What's Next for Oil Prices? Look Out Below!

As with any statistic, though, there’s more than one way to look at the situation. Sure, auto sales are climbing as the economy gets stronger and more Americans hit their local car dealers’ lots. At least to some degree, though, higher auto sales should be expected just as a result of U.S. population growth. And those rising monthly sales figures are masking a continuing trend that is more worrisome for the auto industry: per capita auto sales are still in a long-term decline, even including the solid growth the industry has seen since the end of the recession. Doug Short at Advisor Perspectives did the math and made a graph:

According to Short’s analysis, the peak year for per capita auto sales in the U.S. was 1978. As the red line in the graph shows, the trend is negative since then.

In the graph, per capita auto sales in January, 1976, were defined as 100; the readings in the index since then are relative to that 1976 sales level. As you can see, the index moves higher until August of 1978, when per capita auto sales were up nearly 20 percent over 1976. Since then, per capita auto sales have fallen, reaching a low in 2009 that was nearly 50 percent lower than 1976. Since 2009, per capita auto sales have risen nicely, but are still more than 15 percent below peak.

What could explain the negative trend? Two factors come to mind. First, demographics. It has been widely reported that the millennial generation is less interested in owning cars for a variety of reasons, ranging from a weak economy to a cultural shift away from suburban life. However, the data on millennial car purchases is ambiguous; recently, millennials have started buying cars in volumes that look a lot like their elders. And even if millennials are less interested in buying cars, their preferences can’t explain a shift that began in the 1970s, before they were born.

Related: U.S. Companies Are Dying Faster Than Ever

The other factor that may explain the trend is income inequality. A study of car ownership by the Carnegie Foundation found that countries with higher income inequality have fewer cars per capita. The logic is simple: As more income is claimed by the wealthy, there’s less to go around for everyone else. And that means there’s less money for middle and lower income groups to buy and maintain automobiles, among other things.

Here’s a chart of the Gini index for the U.S. since 1947. (The Gini Index is a widely-used measure of income inequality. A higher Gini number means higher inequality.) Note that the Gini reading started climbing in the late ‘70s – the same time when per capita car ownership in the U.S. began to fall.

This chart tells us, not for the first time, that the U.S. has experienced more income inequality since the 1970s. Combined with the per capita auto sales data above, it suggests that as the rich have gotten richer and everyone else has struggled to keep up, car ownership has suffered. Although this is by no means proof of the relationship between income inequality and per capita car ownership over the last 40 years, it hints at an interesting theory – and suggests that the auto industry has good reason to be concerned about growing inequality in the U.S.

Top Reads From The Fiscal Times:

- 6 Reasons Gas Prices Could Fall Below $2 a Gallon

- Hoping for a Raise? Here’s How Much Most People Are Getting

- What the U.S. Must Do to Avoid Another Financial Crisis

Trump and Schumer Will Try to Scrap the Debt Ceiling

The president and the Senate Democratic leader agreed to seek out a more permanent debt ceiling solution that would end the perpetual cycle of fiscal standoffs. “There are a lot of good reasons to do that, so certainly that’s something that will be discussed," Trump said Thursday. It might not be easy, though, as conservatives see the borrowing limit as a way to keep government spending in check. Paul Ryan said Thursday he opposes doing away with the debt ceiling.

Is a Fix for Obamacare Taking Shape?

Senators on the Committee on Health, Education, Labor and Pensions heard from governors Thursday in the second of four scheduled hearings on stabilizing Obamacare. The common theme emerging from the testimony was flexibility: "Returning control to the states is prudent policy but also prudent politics," said Utah Gov. Gary Herbert, a Republican. He was joined by Democrat John Hickenlooper of Colorado, who said that states need room to innovate and learn from their mistakes. Much of what the governors said was in line with what the Senate panel is already considering, including the continuation of cost-sharing subsidies to insurance companies. (CBS News, Axios)

Senate Approves Trump's Deal with Dems. Will the House Go Along?

The Senate on Thursday voted to fund the government and increase the federal borrowing limit through December 8 as part of a deal that also included $15.25 billion in hurricane disaster relief funding and a short-term extension of the National Flood Insurance Program. The bill passed by a vote of 80-to-17, with only Republicans voting against the bill.

The package now goes back to the House, where it likely faces more strenuous resistance. The Republican Study Committee, a conservative caucus with more than 155 members, on Thursday announced it opposed the deal because it does not include spending cuts. Rep. Mark Walker, the group's chairman, sent a letter to House Speaker Paul Ryan listing 19 policy changes to "address the growing debt burden" or "begin draining the swamp" that could win conservative support for raising the debt ceiling. Some Democrats may also vote against the deal to signal their frustration with an agreement that they say weakened their hand in trying to protect undocumented immigrants who were brought into the country as children.

White House Backs Off Shutdown Threat…for Now

“Believe me, if we have to close down our government, we’re building that wall,” President Trump said of his planned border wall with Mexico 10 days ago. Just two days later, though, White House officials told Congress that a short-term spending bill to fund the government into December wouldn’t have to include $1.6 billion for the wall, The Washington Post reports.

Trump still wants money for the wall to be included in a December budget bill, and he could follow through on his shutdown threat at that point. For now, though, an agreement on a “continuing resolution” to keep the government running after September 30 seems likelier, allowing Congress to deal with some of the other pressing issues it faces this month.

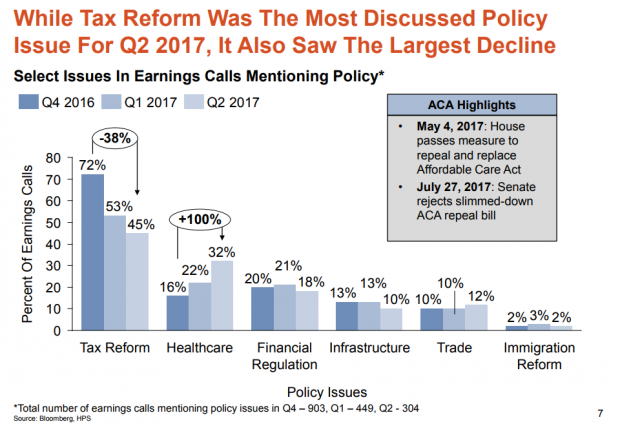

Which Trump Agenda Items Are Companies Talking About With Wall Street?

Hamilton Place Strategies, a public affairs consulting firm, analyzed transcripts of earnings calls by publicly traded U.S. companies over the last three quarters. They found that tax reform was the policy issue companies discussed most on those calls with Wall Street analysts — but that mentions of the subject dropped by 38 percent from the fourth quarter of 2016 to the second quarter of 2017. Overall, the percentage of earnings calls mentioning government or policy issues fell from 41 percent to 16 percent. Health-care reform saw the largest increase.

Does this mean that businesses have given up on tax reform this year? Perhaps. More likely, it's simply the result of a lack of action on the tax overhaul. Hamilton Place notes that mentions of tax policy peaked in February just after the Senate Finance Committee advanced Treasury Secretary Steven Mnuchin's nomination and have spiked after other tax-related announcements. So mentions of tax reform on earnings calls could surge again the fall.

One other note about what businesses have been discussing: Calls mentioning President Trump fell by 84 percent from January to late August.

08312017_HPS_Chart_of_the_day.PNG