Trump Diverting $3.6 Billion from Military to Build Border Wall

The Department of Defense has approved a plan to divert $3.6 billion to pay for the construction of parts of President Trump’s border wall, Defense Secretary Mark Esper said Tuesday. The money will be shifted from more than 100 construction projects focused on upgrading military bases in the U.S. and overseas, which will be suspended until Congress provides additional funds.

In a letter addressed to Senator James Inhofe, chair of the Armed Services Committee, Esper said that in response to the national emergency declared by Trump earlier this year, he was approving work on 11 military construction projects “to support the use of armed forces” on the border with Mexico.

The $3.6 billion will fund about 175 miles of new and refurbished barriers (Esper’s letter does not use the term “wall”).

Esper described the projects, which include new and replacement barriers in San Diego, El Paso and Laredo, Texas, as “force multipliers” that, once completed, will allow the Pentagon to redeploy troops to high-traffic sections of the border that lack barriers. About 5,000 active duty and National Guard troops are currently deployed on the border.

Months in the making: Trump’s declaration of a national emergency on the southern border on February 15, 2019, came in the wake of a showdown with Congress over funding for the border wall. The president’s demand for $5.7 billion for the wall sparked a 35-day government shutdown, which ended when Trump reluctantly agreed to a deal that provided $1.375 billion for border security. By declaring a national emergency, Trump gave the Pentagon the legal authority to move billions of dollars around in its budget to address the purported crisis. Legal challenges to the emergency declaration are ongoing.

Conflict with lawmakers: Congress passed a resolution opposing the national emergency declaration in March, prompting Trump to issue the first veto of his presidency. Democrats on the House Appropriations Committee reiterated their opposition to Trump’s move Tuesday, saying in a letter, “As we have previously written, the decision to take funds from critical military construction projects is unjustified and will have lasting impacts on our military.”

Majority Leader Steny H. Hoyer was more forceful, saying in a statement, "It is abhorrent that the Trump Administration is choosing to defund 127 critical military construction projects all over the country … and on U.S. bases overseas to pay for an ineffective and expensive wall the Congress has refused to fund. This is a subversion of the will of the American people and their representatives. It is an attack on our military and its effectiveness to keep Americans safe. Moreover, it is a political ploy aimed at satisfying President Trump's base, to whom he falsely promised that Mexico would pay for the construction of an unnecessary wall, which taxpayers and our military are now being forced to fund at a cost of $3.6 billion.”

A group of 10 Democratic Senators said in a letter to Esper that they “are opposed to this decision and the damage it will cause to our military and the relationship between Congress and the Department of Defense.” They said they also “expect a full justification of how the decision to cancel was made for each project selected and why a border wall is more important to our national security and the well-being of our service members and their families than these projects.”

Politico’s John Bresnahan, Connor O'Brien and Marianne LeVine said the diversion will likely be unpopular with Republican lawmakers as well. Republican Senators Mike Lee and Mitt Romney expressed concerns Wednesday about funds being diverted from their home state of Utah. "Funding the border wall is an important priority, and the Executive Branch should use the appropriate channels in Congress, rather than divert already appropriated funding away from military construction projects and therefore undermining military readiness," Romney said.

The Pentagon released a list of construction projects that will be affected late on Wednesday (you can review a screenshot tweeted by NBC News’ Alex Moe here).

An $8 billion effort: In addition to the military construction funds and the money provided by Congress, the Trump administration is using $2.5 billion in drug interdiction money and $600 million in Treasury forfeiture funds to support the construction of barriers on the southern border, for a total of approximately $8 billion. (More on that here.)

The administration reportedly has characterized the suspended military construction projects as being delayed, but to be revived, those projects would require Congress approving new funding. House Democrats have vowed they won’t “backfill” the money.

The politics of the wall: Trump has reportedly been intensely focused on making progress on the border wall, amid news that virtually no new wall has been built during the first two and a half years of his presidency. Speaking to reporters at the White House Wednesday, Trump said that construction on the wall is moving ahead “rapidly” and that hundreds of miles will be “almost complete if not complete by the end of next year … just after the election.”

This Is the Most Annoying Thing About Customer Service

The number of Americans fed up with lousy customer service is decreasing but there are still some practices that irritate nearly everyone, according to a newly published report in Consumer Reports’ September issue.

There was a tie for the top customer service complaint. Seventy-five per percent of shoppers surveyed were annoyed by the inability to get a live person on the phone and by dealing with a representative who was rude or condescending.

Seventy-four percent of consumers said they were highly annoyed at being disconnected from a customer service rep, and 71 percent were dissatisfied that they’d been disconnected and then unable to reach the same representative again.

“Many companies today are simply awful at resolving customer protections, despite investments in whiz-bang technologies and considerable advertising about their customer focus,” Scott Broetzman, president of Customer Care Measurement & Consulting, told the magazine.

In a separate report released this week, 24/7 Wall Street found that Amazon.com is the best big company for customer service, followed by Chick-fil-A and Apple. The companies in the publication’s “Customer Service Hall of Shame” include Bank of America, DirectTV and Comcast.

In order to get the best possible customer service, Consumer Reports recommends using the phone, rather than email; showing—and asking for—empathy; and escalating when necessary.

The magazine also suggests putting technology to work. The website Dial a Human can help find the best customer service number for a company, and the service Lucy Phone lets you enter a company’s name and number and then calls you when a rep becomes available so you don’t have to wait on hold.

Top Reads From The Fiscal Times:

- The Next Debt Crisis Could Be Much Worse than in 2013, GAO Warns

- The New Generation of ‘Genuinely Creepy’ Electronic Devices

- Who Are These People Giving Money to Donald Trump?

The Weakest Economic Recovery Since World War II Putters Along

New GDP data released today shows an economy that continues to grow, though at a disappointingly moderate pace.

The good news is that GDP growth picked up after the weak, snow-encrusted first quarter of 2015, when the economy eked out a 0.6 percent growth rate. The bad news is that growth was expected to hit a 2.5 percent rate or better in the second quarter, but initial estimates arriving today pegged that rate at 2.3 percent. Over the first six months of the year, the economy has expanded at an annual rate of 1.5 percent.

The U.S. recession officially ended in the second quarter of 2009. Since then, growth has been relatively steady but lackluster. Compared to other recoveries since the end of World War II, the current recovery is notably weak – without question the weakest of the bunch. The average annual growth rate from 2011 through 2014 was 2.0 percent, based on updated figured released today.

Economists have argued about the causes — a glut of capital, excessive regulation, the domination of finance, low wages driving weak demand — but the simple fact remains: This is a feeble recovery.

This graphic we produced on the Federal Reserve Bank of Minneapolis’s website tells the story – look for the bright red line:

Top Reads from The Fiscal Times:

- The Kids Aren't Alright: More Millenials Are Living with Their Parents

- How Millenials Could Damage the U.S. Economy

- The Pain the Job Numbers Don’t Show

The Shocking Secret About How Your Car Insurance Rate Gets Set

Most drivers probably know that if they get into an accident, their insurance rates are also likely to take a hit. But a new analysis by Consumer Reports finds that your car insurance premiums are increasingly based on factors such as your credit score that are unrelated to your driving record.

How well you drive may actually have little connection to how much you pay for insurance, the consumer group found.

In a two-year investigation, Consumer Reports analyzed more than 2 billion insurance price quotes obtained from more than 700 insurers across the country. It found that in many states a bad credit history will drive up your insurance premiums more than a drunk driving conviction.

“What we found is that behind the rate quotes is a pricing process that judges you less on driving habits and increasingly on socioeconomic factors,” the consumer organization reports. “These include your credit history, whether you use department-store or bank credit cards, and even your TV provider. Those measures are then used in confidential and often confounding scoring algorithms.”

Consumer Reports says it found that most car insurance companies use about 30 elements of the nearly 130 available in a credit report to construct their own secret score for policyholders, and that credit scores could have more of an impact on premiums than any other factor. Drivers with the best credit scores were charged up to $526 less than similar drivers with only “good” scores, depending on where they lived. Only three states — California, Hawaii and Massachusetts — prohibit insurers from factoring in credit scores when setting prices.

Drivers are legally required to carry car insurance, but the lack of pricing transparency makes it harder for them to make informed decisions about which policy to buy. “Because insurance companies are under no obligation to tell you what score they have cooked up for you, you have no idea whether you have a halo over your head or a bull’s-eye on your back for a price increase,” Consumer Reports says.

Industry advertising that promotes special discounts, such as for bundling home and car insurance, only muddles the purchasing process because those special deals don’t actually save people much money, Consumer Reports found.

The organization says it’s high time for truth in car insurance, and it’s asking consumers to sign a petition demanding that insurers -- and the state regulators who oversee them -- use price-setting practices that are tied to more meaningful factors, like driving records. It is also asking consumers to tweet the National Association of Insurance Commissioners, @NAIC_News, and tell them to “Price me by how I drive, not by who you think I am! #FixCarInsurance.”

For more information on state-by-state insurance premiums, or to sign the Consumer Reports petition, go to ConsumerReports.org/FixCarinsurance.

Top Reads From The Fiscal Times:

- Americans Are About to Get a Nice Fat Pay Raise

- How Millenials Could Damage the U.S. Economy

- The Pain the Job Numbers Don’t Show

The Kids Aren’t Alright: More Millennials Are Living with Their Parents

Pity the millennial, poster child of the Great Recession. A popular meme portrays the typical millennial as a basement-dwelling economic loser, forever condemned to live in the nether regions of his parent’s house. Unfortunately, that meme is not without basis. The recession seem to have hit millennials particularly hard, making it even more difficult for young people to find good jobs and to establish their own households.

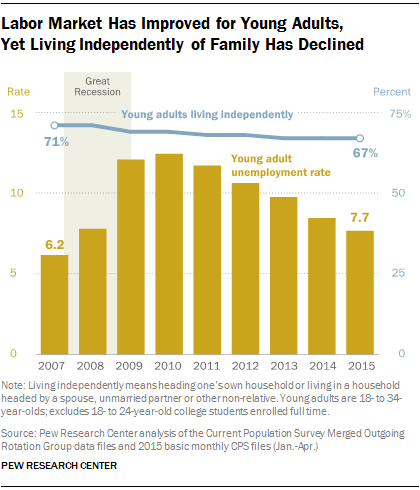

In some respects, things are looking up for millennials. The U.S. job market is strengthening, making it easier to find work, and wages are starting to creep higher. The unemployment rate for young adults (ages 18 to 34, excluding full-time college students) has been heading lower since peaking near 12 percent in 2010; the latest unemployment reading for millennials is 7.7 percent.

However, there is one notable sticking point, and it echoes that basement-dwelling meme. Even though household formation rates have rebounded overall, millennials are still not moving out and establishing their own households like they used to. In fact, more millennials are living with parents or relatives than before the recession, according to new research from Pew.

In 2007, before the recession hit, 71 percent of millennials were living independently. In 2015, that number has fallen to 67 percent, with no sign of bottoming.

On the flip side, 22 percent of young adults were living in their parents’ homes in 2007. That number has risen to 26 percent this year.

The Pew report doesn’t look at why millennials are sticking so close to home. However, it does suggest that the relatively simple economic argument about the lack of good jobs no longer tells the whole story. Since the economy is recovering, however unevenly, there are likely other factors in play. One could be cultural: More young people simply enjoy living at home and are in no hurry to move out. Perhaps the U.S. is becoming more like Italy, where adult children often live at home until they marry.

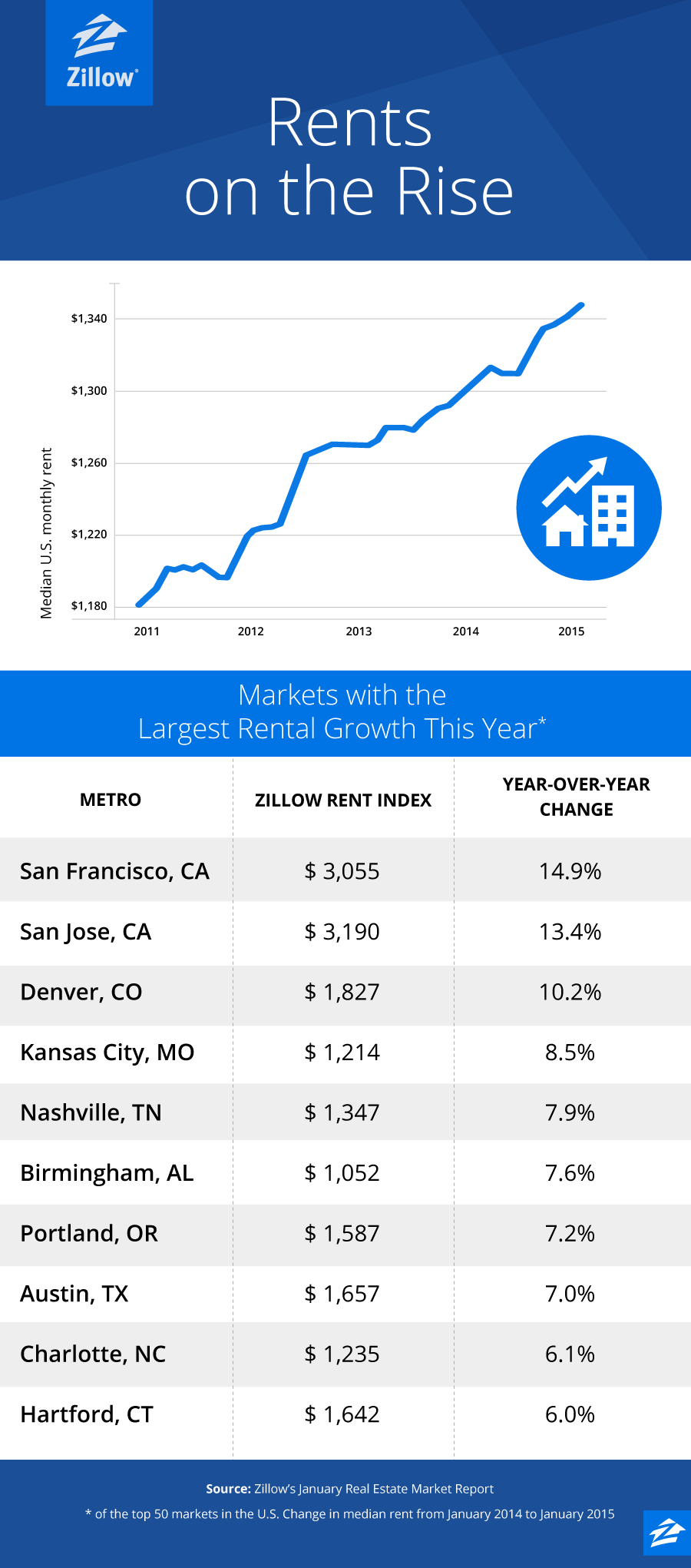

That’s not to say that money plays no role in the trend, though. One big economic factor not addressed in the Pew report is pretty basic: rising rents. This graphic from Zillow makes it clear that rents have been soaring all over the country. More than $3,000 for a one bedroom in San Francisco? With those kind of numbers, living at home makes all the sense in the world.

DOJ Indicts Democratic Lawmaker for Corruption

Martin Matishak, The Fiscal Times

The Justice Department has indicted Rep. Chaka Fattah (D-PA) on almost 30 federal counts of political corruption.

The 11-term congressman and four associates were indicted on 29 federal charges, including bribery, money laundering, falsification of records, and multiple counts of bank and mail fraud, the department announced Wednesday.

Related: Billions in Unfinished Business as Congress Heads Out for Vacation

The charges against Fattah and his associates stem from his failed run for Philadelphia mayor in 2007.

Fattah and the others "embarked on a wide-ranging conspiracy involving bribery, concealment of unlawful campaign contributions and theft of charitable and federal funds to advance their own personal interests,” according to Assistant Attorney General Leslie R. Caldwell.

Justice alleges that Fattah borrowed $1 million from a wealthy donor during his mayoral bid and that he returned $400,000 in unused funds and developed a scheme to repay the remaining $600,000 by tapping charitable and federal grants through a local non-profit the Pennsylvania lawmaker created.

Federal officials also allege that the Fattah sough to repay supporters by offering federal grants and used funds from both his mayoral and congressional campaigns to pay down his son's student loan debts of around $23,000.

"Public corruption takes a particularly heavy toll on our democracy because it undermines people’s basic belief that our elected leaders are committed to serving the public interest, not to lining their own pockets,” she said in a statement.

House Minority Leader Nancy Pelosi (D-CA) said that Fattah has stepped down as the top Democrat on the House Appropriations Commerce, Justice, Science and Related Agencies subcommittee.